4 min read

Blog

Starting in 2026, the social security contribution calculation baselines in Germany will be redefined. This adjustment is more than a formality – it has a direct impact on personnel planning, budgeting, and cost management in companies. This means, especially for HR and finance teams, that the previously used blanket assumptions regarding social security contributions are being called into question.

Why the 2026 redefinition is particularly relevant

The assessment ceilings determine the income up to which employers pay contributions to health, long-term care, pension, and unemployment insurance. With the planned redefinition, these limits will be adjusted to reflect wage developments – which in many cases leads to increasing employer contributions.

Companies with many higher-paid roles will feel the effects particularly strongly. At the same time, the changes offer an opportunity to make budgeting processes more precise and transparent. Knowing your actual social security costs allows you to manage investments in personnel more effectively and avoid miscalculations.

Away from the flat rate – towards precise planning

As the article Why Accuracy is Crucial in Headcount Budgeting describes, the use of flat social charge rates – such as a uniform percentage for all employees – is risky and imprecise. It can lead to over- or under-budgeting, which in turn limits the ability to act in personnel planning.

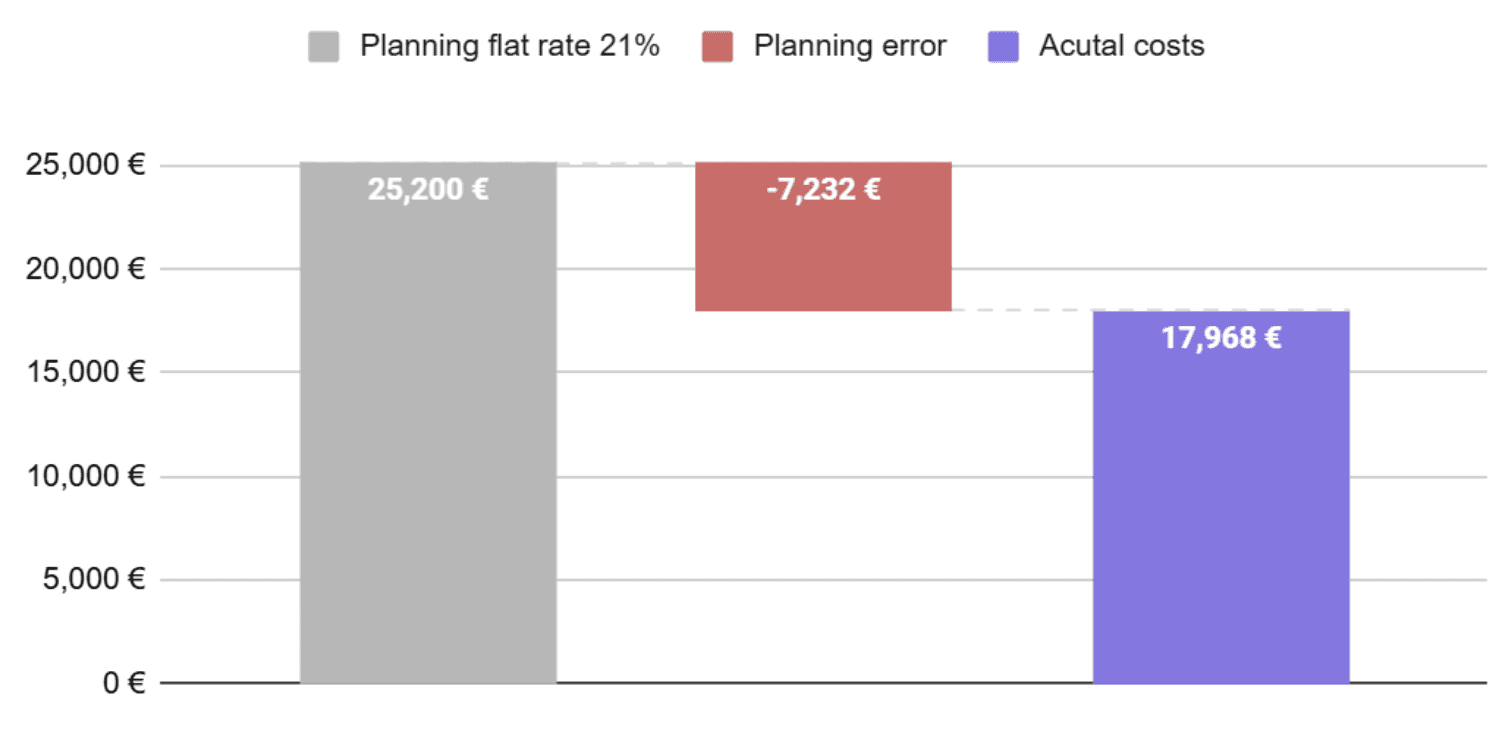

The following example highlights how planning with a flat rate massively blurs your budgets. For an annual compensation of €120k, using a 21% flat rate leads to a planning error of 7,232€ - a deviation of >40% of the actual costs.

Especially in light of the new assessment thresholds, companies should switch to granular and data-driven models. Useful approaches include:

Segmenting the workforce by salary level, employment type, and location,

Considering variable compensation components (OTE) in cost planning,

and the use of specialized software solutions that automatically incorporate current legal frameworks.

This allows for realistic simulation of social security costs – a decisive advantage when contribution rates or assessment limits change.

Impact on Headcount Budgeting and Workforce Strategy

For HR and Finance teams, the reform offers an opportunity to view social security contributions not as a rigid secondary factor, but as a dynamic cost factor. Companies that plan precisely can use their headcount budgets more efficiently and make more informed decisions – for example, when considering whether new hires in certain salary ranges or regions make economic sense.

The 2026 revision is therefore also a wake-up call to question existing assumptions about employer costs. Those who address the changes early on will gain clarity about future burdens – and scope for forward-looking HR policies.

Conclusion

The new social security assessment bases from 2026 underline the importance of precise planning and transparency regarding social security contributions. Companies that use the transition to refine their models and implement modern tools will benefit in the long run: through better budget control, reduced risk, and strategically sound workforce planning.

➡️ Learn more about why accurate social charge planning is crucial for employers in the article Why Accuracy in Social Charge Planning is Crucial

All your people data in one place

English

© 2026 Basqo. All rights reserved.